How Market Crashes Affect Investment Growth: The Truth about Long-Term Investing

- Ling Zhang

- Feb 7

- 4 min read

Investment Growth Myths Exposed: Why Long-Term Investing Alone Isn’t Enough

The four most dangerous words in investing are: ‘This time it’s different.’— Sir John Templeton

Investing for the long term is often touted as a foolproof strategy, with many believing that staying in the market guarantees strong returns. While time is indeed a crucial factor in wealth accumulation, historical market crashes have shown that time alone is not a guarantee of positive returns. The period from 2000 to 2024 provides critical insights into how market risks can impact 401(k) investments and why diversification is the key to financial stability.

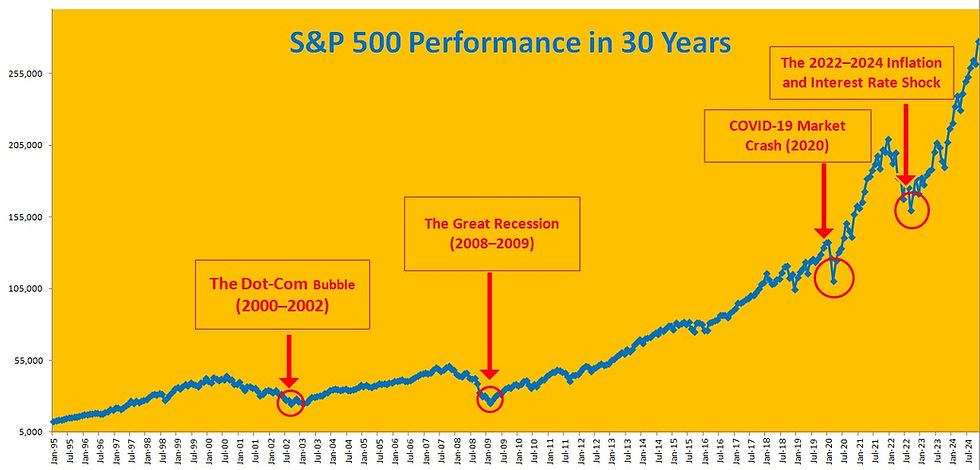

1. Major Market Crashes and Their Impact on 401(k) Investments

· The Dot-Com Bubble (2000–2002)

At the turn of the millennium, the rapid rise and fall of tech stocks led to a significant market downturn. The S&P 500 dropped nearly 50% from its peak, wiping out years of gains. Investors who were heavily invested in tech stocks saw their portfolios suffer immense losses, and those who failed to rebalance their portfolios took years to recover.

· The Great Recession (2008–2009)

Just as markets recovered from the dot-com crash, the 2008 financial crisis triggered another massive downturn. The S&P 500 plunged over 50% in just over a year. Many investors nearing retirement saw their 401(k) balances cut in half, forcing them to delay retirement or return to the workforce. Those who had a well-diversified portfolio with safer assets, such as bonds or annuities, fared much better.

· COVID-19 Market Crash (2020)

In early 2020, the pandemic caused a rapid market sell-off, with the S&P 500 dropping by 34% in just over a month. While the market rebounded quickly due to stimulus measures and low interest rates, the volatility highlighted how unpredictable markets can be. Investors who panicked and sold their holdings at the bottom missed out on the rapid recovery.

· The 2022–2024 Inflation and Interest Rate Shock

The post-pandemic economic recovery brought about high inflation and aggressive interest rate hikes by the Federal Reserve. These factors led to increased volatility and significant losses in both stock and bond markets, proving that even so-called "safe" investments like government bonds can be risky under certain economic conditions.

2. The Myth: Longer Investment Time Always Guarantees Growth

While historical trends show that markets tend to rise over the long term, prolonged periods of stagnation or losses can severely impact investors. For example:

Investors who started in 2000 had to wait 14 years to break even after the dot-com and Great Recession crashes.

Japan’s stock market (Nikkei 225) took over 30 years to recover from its peak in 1989.

Investors retiring in 2008 saw their 401(k)s cut in half, proving that timing and risk management are crucial.

Relying solely on long-term stock market growth can be risky. A well-balanced strategy must incorporate other asset classes to hedge against downturns.

3. The Solution: Diversification Beyond Stocks

· Mix Asset Classes: A balanced investment portfolio should include:

Stocks: Provide growth but come with high volatility.

Bonds: Offer stability and income, though they can also be impacted by interest rate changes.

Real Estate: A hedge against inflation and market downturns.

Commodities (Gold, Silver, etc.): Protection against economic uncertainties.

Fixed Index Annuities & Cash Equivalents: Provide guaranteed income and safety from market downturns.

· Diversify Across Time Periods: Instead of relying on a single investment period, consider:

Dollar-Cost Averaging (DCA): Investing regularly regardless of market conditions to reduce the risk of poor market timing.

Lifecycle Investing: Adjusting risk exposure based on age and retirement horizon.

· Have a Safety Net:

Keep a portion of your savings in low-risk assets for economic downturns.

Maintain an emergency fund separate from your investment portfolio.

Consider alternative income streams to reduce reliance on market-driven returns.

Market crashes are inevitable, and history has shown that they can significantly impact investment growth, even over extended periods. The belief that “the longer the investment, the greater the return” does not always hold true. The key to financial success lies in diversification—spreading investments across different asset classes and timeframes to mitigate risk.

By learning from past market cycles and proactively managing risks, investors can better protect their 401(k)s and overall financial well-being. Don't rely on time alone—take control of your investment strategy today to secure a more stable and prosperous future.

If you’d like to learn how to build a diversified financial strategy tailored to your goals, 👉 Learn the three cornerstones of building wealth

May you grow to your fullest!

Subscribe Grow to Your Fullest for Financial Tips

*** Please DOWLOAD the FREE document, Find your signature vision questionnaires so you use it to help you find your life vision and mission.

>> Contact Grow to Your Fullest

留言